What Is Key Person Insurance? Benefits, Cover & How It Works

Running a successful business often involves a team of dedicated individuals who contribute their skills and expertise to the company’s growth. But what if one of those key individuals were suddenly unable to work due to illness, injury, or even death? That’s where key person business insurance comes into play. In this blog post, we’ll explore what key person business insurance is, why it’s essential, and what it covers.

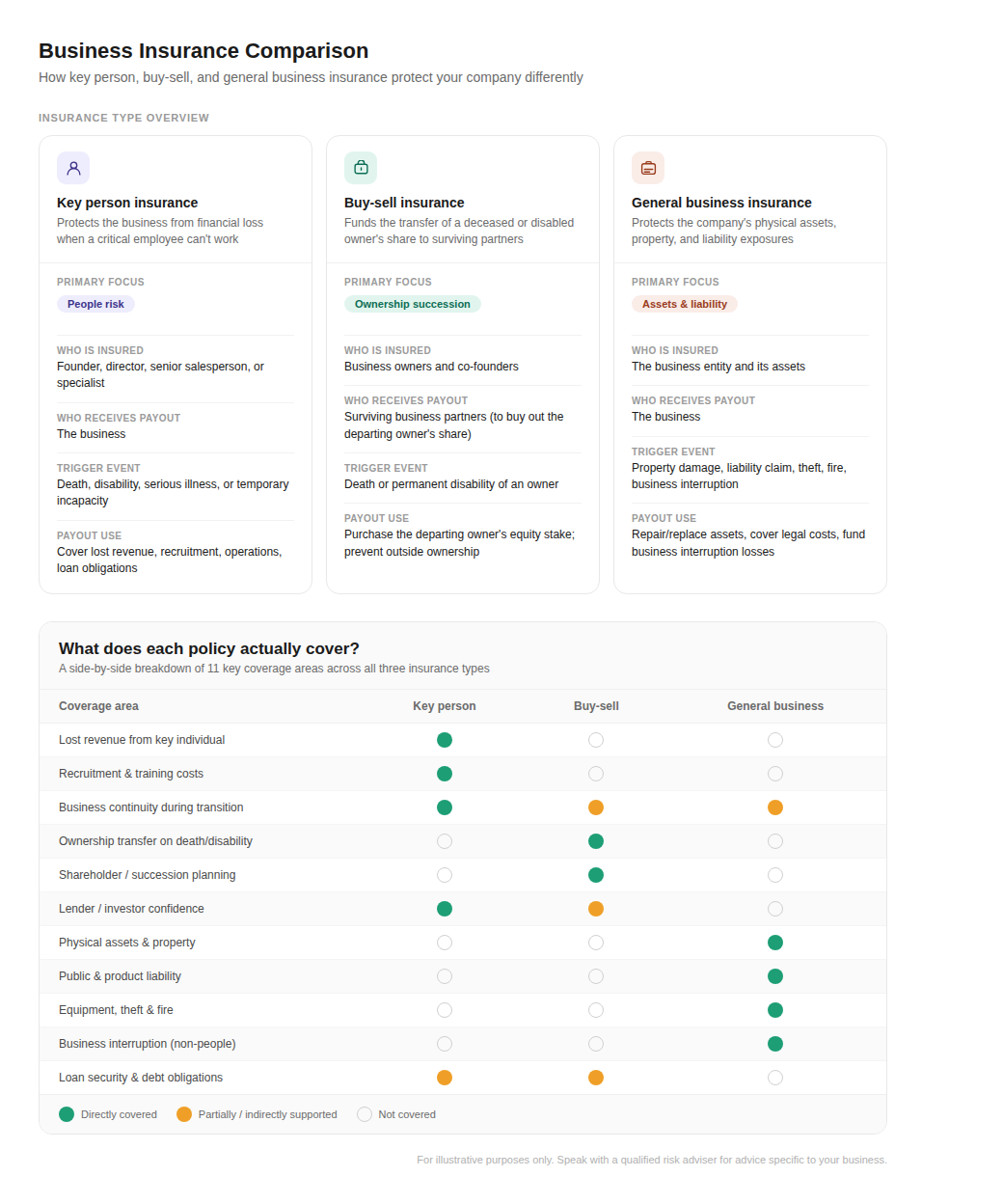

What Is Key Person Business Insurance?

Key person business insurance, sometimes called key person insurance or keyman insurance, helps protect a business if an important team member becomes unable to work due to illness, injury or death. A key person is someone whose knowledge, leadership or relationships play a major role in the success of the business. This could be a founder, director, senior salesperson or specialist employee.

In most cases, the business owns the policy, pays the premiums and receives the benefit if that person can no longer work. The insurance payout can help the business manage financial disruption while it adjusts, whether that means covering lost revenue, supporting operations or recruiting a replacement.

Who Should Consider Key Person Insurance?

While many businesses can benefit from a key person insurance policy, it is especially valuable when certain individuals play a critical role in the company’s success.

- Founders: The health and availability of a founder can have a major impact on the stability of a business. If they are unexpectedly unable to work due to injury, illness or death, integral relationships, operations, and the overall direction of a company can be put in jeopardy. It’s important to structure a strong key person insurance policy relating to founders and owners, as their absence often causes the greatest blow to the longevity of an organisation.

- Sales Director: A sales director or operations manager often holds key relationships with clients and stakeholders, making them an important driver of revenue and growth. If they are unexpectedly unable to work, the business may experience a drop in productivity while a replacement is found or an existing team member steps into the role. Key person insurance can help provide financial support during this transition.

- Specialists: Similar to managers, a specialist team member usually holds invaluable experience and knowledge within a niche component of the organisation. Whether they understand essential systems or utilise a certain skill, they are integral to the company’s ongoing success. While planning ahead and organising key person cover does not replace their expertise, it can be a useful way to mitigate financial loss during the time they are removed from their position.

Benefits Of Key Person Insurance

- Manage cash flow disruptions: The sudden loss of a key person can have significant financial and cash flow consequences for a business. Key person insurance provides a financial safety net, ensuring that the company can continue operating and meeting its financial obligations during a challenging time.

- Loan and credit facilities: Many businesses rely on loans or credit facilities to fund their operations and growth. In some cases, lenders may view key person insurance as an added layer of protection, helping the business maintain access to financing if a key individual is no longer able to contribute to the business.

- Recruitment and training costs: Finding and training a replacement for a key individual can be both time-consuming and expensive. Key person insurance can help cover recruitment costs, training expenses and any additional compensation needed to attract a suitable replacement,

- Providing financial breathing room during restructures: The business may need time to restructure roles, leadership or operations. Insurance can help provide financial breathing room while these longer-term decisions are made.

How Key Person Insurance Can Help Your Business

Beyond providing financial support, this type of cover can help protect the long-term stability of a business. Losing a key individual can create uncertainty for staff, clients, lenders and investors, particularly when that person plays an important role in leadership, revenue generation or operations.

Having a policy in place can help maintain confidence in leadership and reassure investors and lenders that the business has planned for unexpected events. It can also support business continuity planning, helping the organisation navigate the transition if a founder, employee or specialist becomes unable to work due to illness, injury or death. In some cases, the insurance proceeds may also help the business continue meeting important financial or contractual obligations while longer-term solutions are put in place.

Types Of Key Person Insurance Policies

Key person insurance is not a standalone policy. Instead, it is typically structured using different types of insurance cover depending on the risks a business wants to protect against.

- Life Insurance: Provides a lump-sum payment to the business if the insured key person passes away.

- Total and Permanent Disability (TPD) Insurance: Pays a lump sum if the key individual becomes permanently unable to work due to injury or illness.

- Trauma (Critical Illness) Insurance: Provides a lump sum if the key person is diagnosed with a specified serious illness such as cancer, heart attack or stroke.

- Income Protection Insurance: In some cases, income protection may be used to provide ongoing payments if the key person is temporarily unable to work due to illness or injury.

Key Person Insurance Vs Business Insurance

Key person insurance and general business insurance protect a business in different ways. Key person insurance is designed to protect a business from the financial impact of losing an important employee, founder or specialist whose skills, leadership or relationships are critical to the company’s success. If that individual becomes unable to work due to illness, injury or death, the policy can provide a payment to help the business manage the disruption.

General business insurance, on the other hand, is typically designed to protect the company’s assets, property and liability risks. This may include cover for things like equipment, buildings, public liability or business interruption.

While both forms of cover help manage risk, key person insurance focuses on protecting the people who drive the business, whereas general business insurance focuses on protecting the assets and operations of the business itself.

Is Key Person Insurance Right For You?

In today’s competitive business landscape, the success of many companies hinges on the skills and contributions of key individuals. Key person business insurance is a strategic tool that helps protect your business from the financial repercussions of losing such a valuable asset.

Here are a few points to consider if this cover suits you:

- What is your revenue dependency?

- How is your company exposed to debt?

- What difficulties would you face in replacing a key team member?

For many business owners, key person insurance can provide peace of mind and financial stability during unexpected events. While the appropriate level of cover will depend on your business structure, financial commitments and the role of key individuals, it can form an important part of a broader risk management strategy.

If you’re unsure whether this type of cover is right for your business, speaking with a specialist risk adviser can help you assess your exposure and review options that align with your business structure and long-term goals.

Frequently asked questions

Explore the answers to some common questions about insurance policies.

Insurance and superannuation often work best when considered together, as they both play a role in protecting your financial future. Insurance can help provide support if something unexpected happens, while superannuation is focused on long-term planning and retirement. Whether you need one or both depends on your personal circumstances, goals, and stage of life. We take the time to understand your situation and help you decide what level of planning is appropriate for you.

Business key person insurance allows a company to take out an insurance policy on an important employee, owner or director whose role is critical to the business. The business typically owns the policy, pays the premiums and receives the benefit if that person dies, becomes seriously ill or is unable to work. The payout can help the business manage financial disruption and maintain operations while it adjusts to the loss of that individual.

Key person insurance helps provide funds to maintain cash flow, cover recruitment and training costs for a replacement, reassure lenders or investors, and support business continuity. This financial safety net helps companies recover and continue operating during unexpected leadership loss.

Businesses that rely heavily on specific individuals should consider key person insurance. This often includes founders, executives, top salespeople, technical specialists, or anyone whose expertise, relationships, or leadership significantly affects revenue and operations. Small and medium-sized businesses are particularly vulnerable if a key person is lost, making this coverage especially valuable.

The amount of key person insurance a business needs depends on the financial impact the individual has on operations. Companies often estimate coverage based on the person’s contribution to profits, the cost of recruiting and training a replacement, outstanding debts, and potential revenue losses. Many businesses choose coverage equal to several years of the key person’s economic value.

In many cases, premiums for key person life insurance are not tax-deductible because the business is the beneficiary of the policy. However, tax treatment can vary depending on the policy type and local regulations. Businesses should consult a qualified accountant or tax adviser to understand how key person insurance is treated under their jurisdiction’s tax laws.

Calendar

We’re here to help you protect what matters most.

Whether you’re planning for your family, your future, or your business, our team listens, simplifies, and guides you every step of the way.

Reach out and let’s build your peace of mind together.