Income protection insurance is designed to provide a financial safety net when you are unable to work due to illness or injury. However, like all insurance policies, it comes with exclusions and limitations that are important to understand before you commit to a policy. Knowing what isn’t covered can be just as valuable as knowing what is, helping you avoid unexpected surprises when you need your cover the most.

What Is Income Protection Insurance Designed to Cover?

Before exploring the exclusions, it helps to understand what income protection insurance is built to do. At its core, it is designed to replace a portion of your income (typically up to 70% of your pre-disability earnings), if you are unable to work due to a covered illness or injury. This provides ongoing financial support to help you meet everyday living expenses, such as mortgage or rent repayments, utility bills, and other financial commitments, while you focus on your recovery.

Cover is generally paid out as a monthly benefit and continues for a set benefit period, which may range from two years through to age 65, depending on your policy. Most policies also include a waiting period before payments begin, commonly between 14 and 90 days. Income protection is intended to bridge the gap between your last day of work and your return to employment, offering financial stability during what can be a prolonged and stressful period.

What Is Not Covered By Income Protection Insurance?

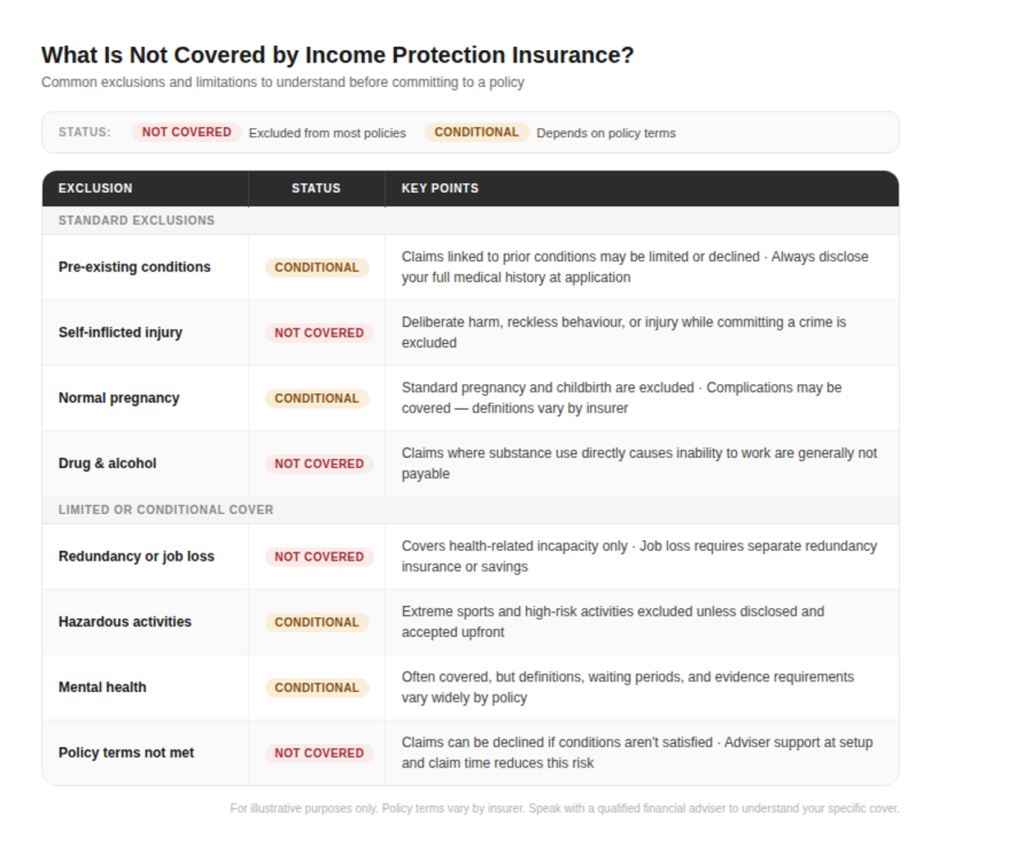

Income protection insurance can be a valuable safety net if you’re unable to work, but it doesn’t cover every situation. Like most insurance policies, there are exclusions you should understand up front.

Pre-existing medical conditions are one of the most common limitations. If you had symptoms, treatment, or a diagnosis before taking out cover, related claims may be reduced or declined. Self-inflicted injuries, caused by reckless behaviour, or that occur during unlawful activities, are also typically excluded.

Standard pregnancy and childbirth are generally not covered, although complications may be included depending on the policy. Similarly, claims linked to drug or alcohol use are often limited, especially where substance use affects your ability to work.

It’s also important to note that income protection doesn’t cover unemployment or redundancy, as it’s designed for health-related work incapacity. Cover for hazardous jobs or high-risk activities may also depend on disclosure and insurer approval.

How To Avoid Gaps In Your Coverage

Understanding the terms of an income protection policy is essential to avoid unexpected gaps in coverage. While policies may appear similar at a glance, the details in the wording can significantly impact how and when you’re paid.

One of the first areas to review is the definition of disability. Some policies only pay if you’re unable to work in any occupation, while others cover you if you can’t perform your specific role.

It’s also important to check the waiting period, which is how long you must be off work before payments begin. Choosing a longer waiting period can reduce premiums, but you’ll need enough savings to cover expenses during that time. Similarly, the benefit period determines how long payments continue, whether that’s a few years or up to retirement age.

Pay close attention to exclusions, partial disability benefits, and any conditions around returning to work. Understanding how income is assessed, especially if your earnings fluctuate, can also prevent surprises at claim time.

Taking the time to read and clarify these terms, ideally with professional guidance, can help ensure your cover genuinely protects you when you need it most.

When Should You Review Your Policy?

Reviewing your income protection insurance regularly is essential to ensure it continues to meet your needs as your circumstances change. A good rule of thumb is to revisit your policy at least once a year, but certain life events should prompt an immediate review.

For example, if your income increases or decreases, your current level of cover may no longer be appropriate. Similarly, major milestones such as starting a new job, becoming self-employed, having children, or taking on a mortgage can all impact the amount of protection you need. If your financial responsibilities grow, your policy should reflect that.

Changes to your health or lifestyle are also important triggers. While you generally can’t update past medical disclosures, reviewing your policy can help you understand how any new conditions might affect future claims. In addition, insurers may update product features over time, so it’s worth checking whether your existing policy still offers competitive benefits.

You should also review your waiting period, benefit period, and any optional extras to ensure they still align with your financial situation and goals. Regular reviews help minimise gaps in coverage and give you confidence that your policy will support you when it matters most.

At Panorama, our advisors are actively reviewing the policies of our clients to ensure they are appropriately covered while also not overpaying, providing peace of mind and a service that has your best interest at heart.

Frequently asked questions

Explore the answers to some common questions about what is not covered by income protection insurance.

Income protection insurance generally excludes pre-existing conditions (whether disclosed or not, depending on the policy), self-inflicted injuries, and illnesses arising from drug or alcohol misuse. It also does not typically cover redundancy or job loss, as it’s designed for health-related inability to work. Some high-risk activities may be excluded unless specifically agreed to within the policy.

Pre-existing conditions are often excluded or limited, especially if symptoms or treatment occurred before the policy started. In some cases, insurers may offer cover after a period without symptoms. It’s important to disclose your full medical history when applying, as non-disclosure can lead to denied claims or reduced benefits later on.

Income protection insurance does not typically cover unemployment or redundancy. It is designed to provide financial support if you are unable to work due to illness or injury. For job loss protection, separate insurance products or emergency savings are usually required.

Many policies do cover mental health conditions such as depression or anxiety, but this depends on the insurer and policy terms. Some policies may include exclusions, waiting periods, or stricter definitions. It’s important to review how mental health is defined and what evidence is required to understand the level of cover provided.

In some situations, a claim may not be paid if the policy terms or conditions aren’t met. This can depend on how the cover is set up and the circumstances around the claim. Taking the time to understand your policy, and working with an adviser who can guide you through both setup and the claims process, can help reduce the risk of issues later on.

Calendar

We’re here to help you protect what matters most.

Whether you’re planning for your family, your future, or your business, our team listens, simplifies, and guides you every step of the way.

Reach out and let’s build your peace of mind together.